Source: http://afr.com/p/business/financial_services/banks_told_to_prepare_for_the_worst_UYmkAZxHukEUAUh9XASsoK

APRA's John Laker wants to know the impact of external crises. Photo: Lee Besford

Australian banks have been ordered to urgently stress test their ability to withstand a sharp rise in unemployment, a ?collapse in the property ?market and economic recession amid rising anxiety over the European debt crisis.

The Australian Prudential Regulation Authority has told banks to model what would happen if the European meltdown spread to Australia through a series of stress tests designed to ensure the strength of the local banking system.

The regulator has given the banks just one week to model the impact of a worst-case scenario resulting in contraction in gross domestic product, an unemployment rate of 12 per cent, as well as a 30 per cent decline in house prices and a 40 per cent drop in commercial property values.

Bank executives told The Australian Financial Review the worst case scenario was extreme and difficult to?model given the short weekend deadline. "We think that's probably part of the test," said one senior banker. "If you can't do this modelling or say you're not sure of the impact, APRA will be onto it."

The stress test has been prompted by an escalation of the European sovereign debt ?crisis that could lead to a global recession and a hard landing in China.

It comes in the same week that the Reserve Bank of Australia's deputy governor, Ric Battellino, warned that Australia's indirect exposure to Europe "through the effect on some of our important trading partners, could be significant".

The European Banking Authority was created in January this year to stress test troubled banks in the region. The EBA released its latest quarterly stress test results earlier this month revising the capital shortfall to ?114.7 billion ($151 billion).

The short notice and time frame allowed by APRA, particularly in light of negative comments from the RBA, indicates the regulator is ?preparing for a difficult 2012.

Bank sources say there is no suggestion APRA is concerned about existing credit quality and assessment. Rather, the authority is seeking to understand the impact of a severe external shock. The APRA missive has had bank treasurers and risk officers scrambling in a week in which three of the big banks held annual meetings.

Australia's banks have limited exposure to Europe, totalling $87.2?billion, or 2.7 per cent of assets, according to the RBA. Of that amount, $74.6 billion is exposed to borrowers in core nations - France Germany and the Netherlands - mostly to banks.

APRA, which declined to comment, has conducted stress tests on Australia's banks in the past, as have international agencies and credit raters.

In 2003, the regulator tested the banks' resilience to a sharp fall in house prices. It concluded that while Australia's banks could withstand a sharp fall in property values, mortgage insurance providers would struggle to withstand claims.

APRA again tested the banks in 2005 and 2006 to determine their ability to withstand a three-year stressed scenario where unemployment rose to 8.75 per cent as house prices fell by 30 per cent.

While profits would decline as bad debts and funding costs increased, the banks would not lose money and could withstand a short, sharp downturn because of their larger weighting to mortgages.

APRA did not discuss or make the findings public until long after the tests were conducted.

In recent months, independent stress tests have been conducted on the Australian banks in response to overseas investors' concerns that Australia's high property prices and elevated levels of indebtedness left the nation's lenders exposed to a bursting of the housing bubble.

In January this year, Fitch Ratings conducted an independent stress test on Australia's big four banks.

Fitch concluded that, in the event of a severe property downturn, the banks would be hit with cumulative losses of $6 billion and a 25 per cent decline in operating profit over three years.

Credit analysts at investment bank Deutsche Bank also conducted an impact study on the major banks whereby mortgage defaults rose by 9?per cent and housing prices fell by 30 per cent.

Deutsche Bank concluded the banks were unlikely to experience losses of more than $8 billion.

Both tests showed that low loan-to-value ratios, or the high level of equity within mortgages, provided a buffer in the event of house prices falling sharply.

APRA's latest test is clearly based on a worst-case scenario because it does not allow the banks to assume any management mitigation.

Bankers believe the regulator will request modelling of a second and even third scenario.

"For example, the first round assumes no write-offs of bad debts, which means you can't realise any tax losses, leaving you with a deferred balance sheet asset but no capital relief," one risk officer said.

"That's not realistic and it guarantees them a bad outcome, but then we would expect APRA to work backwards to see what impact mitigation measures by management might have. This first wave though is a pretty raw, theoretical piece of work."

with John Kehoe

The Australian Financial Review

^^^Prices are already down a long way from the peak in WA.

If there was a further 50% decrease it would most probably be bad for everyone - including people who don't own houses - as it would send a tidal wave of bad debt through our economy.

About 6 months ago, Colin Barnett was saying something about the expectations of first home buyers being too high - want much more than previous generations, bigger, better locations, brand new or fully reno'd etc etc... It was some interesting food (EDIT: for thought... to jam up his arse...)

Barnett can jam it. I found that comment offensive as due to negative gearing and mining boom pushing up prices, I can't afford a piddly 3x1 with no fruit, in an average area - and I am a high income earner.

Yes some people want way too much but he needs to realise it is a bit different to when he bought his first home

Ive seen 3 X 1's around for under $350k at the moment relatively close to the coast, for a high income owner with a 20 % deposit that should be affordable. The trick is the 20% deposit!

If anybody thinks now is the right time for high risk investment, I suggest you consult a psychiatrist.

Yanchep 3x2 home and land package $320,000.00 close to the beach versus City Beach same situation same house (older) $1,500,000.00???? That leaves a lot of spare cash to be 1 hour away from the city! You can then use a little bit of that spare cash to buy a very comfortable car to commute!![]()

^^^ Still depends on where you live vs median housing prices.

The small city where I live has the highest average wage in Vic (or used to, due to the Alcoa Smelter & subtrades, crayfishing & the Port), but you can easily buy a nice 3 or 4 bed brick veneer home for <300k. Still >3 years salary, but affordable, and near beach/city centre/pubs/schools etc. There are a few places here for sale >1mill - although this place is about as cheap as a coastal city with all the benefits gets.

(P.S. The 'Average' Vic salary is still less than $70k, and there are many of us that earn well-under that...and to be honest, we can live comfortably on that sort of coin - no complaints here.![]() )

)

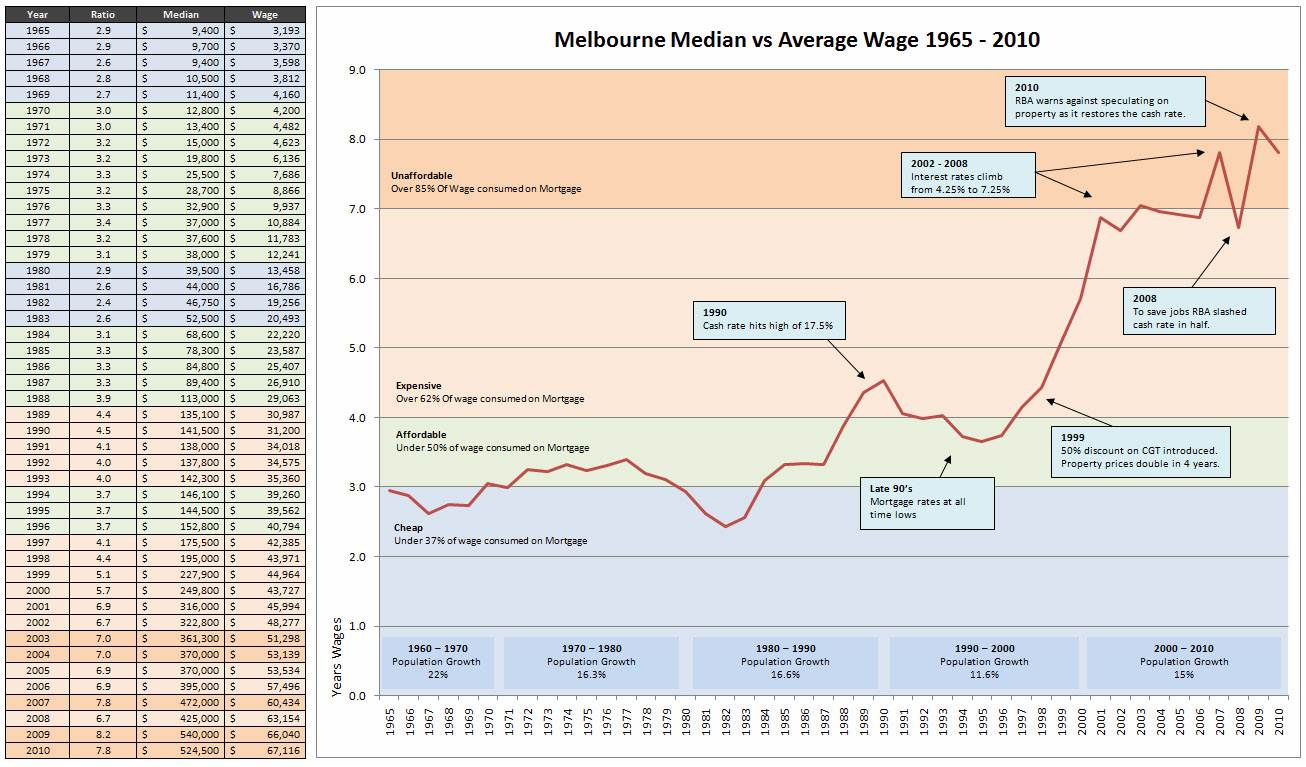

K Dog love your numbers and graph. What is the source?

Story would have to be the same (or somewhat worse) for Sydney, right?

From wiki:

Real Estate Bubble section.

en.wikipedia.org/wiki/Real_estate_bubble

Check out the population growth chart:

en.wikipedia.org/wiki/Australian_property_bubble

It's when people start to owe more on their home than they can get for it on the market that it will start to go pear shaped.

There are signs of that happening now.

www.theage.com.au/business/new-reality-owing-more-than-you-own-20111221-1p4l2.html

Pay off those debts, and buckle up.